24/02/2026

Latest data reveals mortgage holders easing off debt reduction to rebuild savings. This gives brokers a clear chance to guide clients with offset accounts, cashflow planning and flexible loans in a shaky rate market.

Early signals for 2026 reveal a subtle but significant pivot in borrower behaviour that every mortgage broker needs to understand. According to the latest Consumer Pulse survey from Agile Market Intelligence, mortgage holders are dialling back their singular focus on repayments, with the share ranking debt reduction as their top priority slipping from 71% in December to 62% in February. Meanwhile, savings have jumped fast and nearly one in three now call it their number one goal, up to 29% from 21% over the same period. The survey, tracking household priorities through early 2026, captures a market that’s stabilising after late 2025 rate cuts but bracing for the RBA’s fresh 0.25 percentage point hike in February.

The Data That Brokers Can’t Ignore

This change makes perfect sense from a broker’s lens. Rate drops in the second half of last year gave households breathing room to redirect surplus cash from extra repayments into emergency funds. Even with living costs still high, the numbers tell a clear story. Nationally, the picture broadens further: 47% of all respondents prioritise savings, edging out day-to-day expenses at 27% and debt repayment at 26%. Among mortgage clients specifically, everyday costs remain at just 9%, underscoring that the main pull is between sticking to debt rules and stacking cash buffers. From a broker perspective, this isn’t just data but a roadmap to repositioning your value proposition beyond rate-chasing.

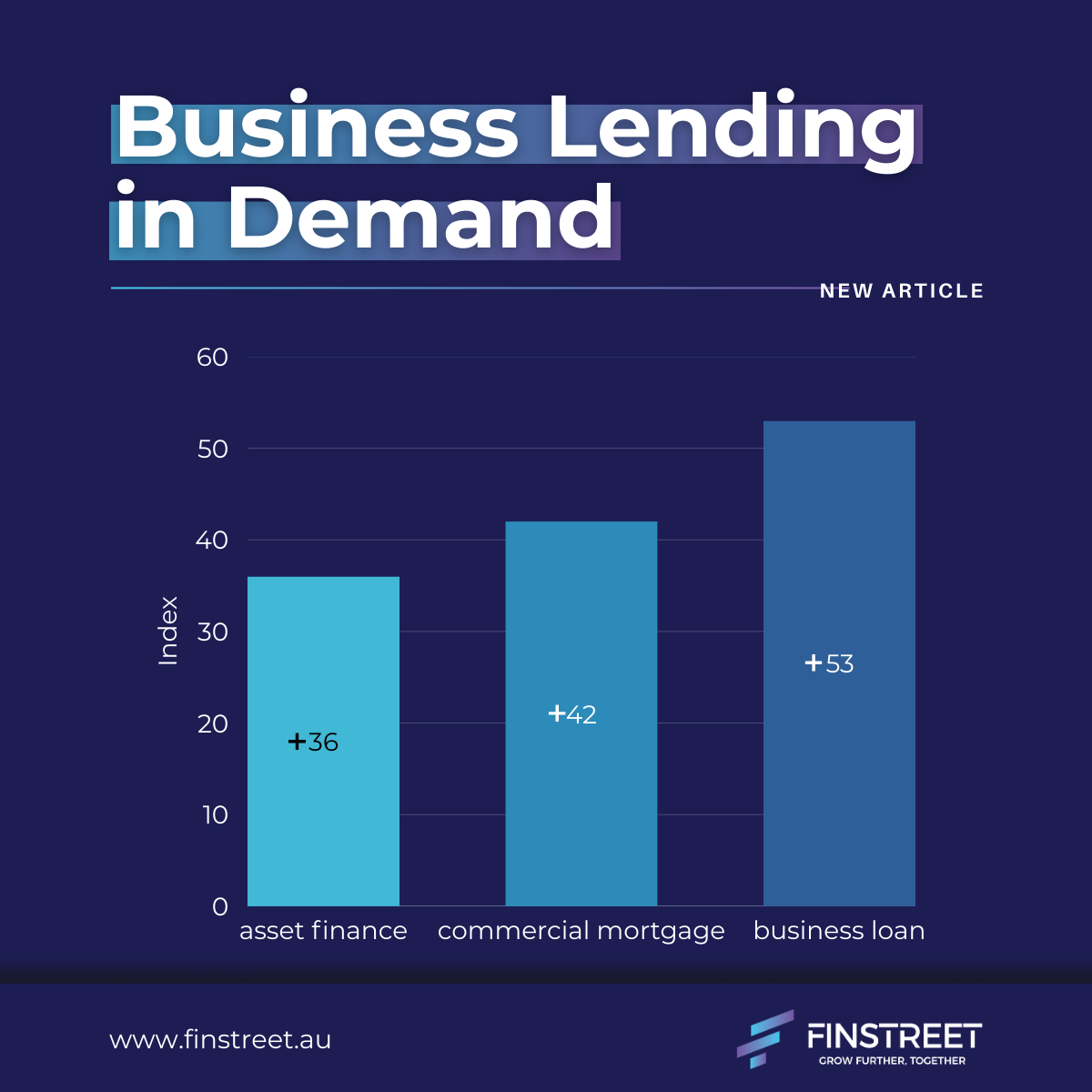

Business lending momentum may dominate headlines, but this consumer pivot carries equal weight for residential brokers. Mortgage clients still pay loans, but further from that, they want plans that last. Mortgage clients are also leaning into flexible tools like offset accounts and redraw facilities that let them toggle between aggression and caution. The market demand here stays even, and brokers win big by offering clients plans that match changing needs, not fixed loans that trap people.

Brokers Must Lead the Pivot

What this means for brokers in 2026 is simple. Demand for refinancing hasn’t evaporated, but it’s evolving toward holistic cashflow conversations. At core, clients seek three things: certainty on minimums, flexibility for surplus, and clarity on trade-offs.Show them the math: extra repayments shave principal but tie up funds; offsets deliver interest relief with instant access. Embed a “two-bucket” review framework: mandatory repayments in one, strategic surplus in the other.

Segment your approach for maximum impact. Households deep in mortgages (62% still repayment-focused) need strong offset loans and split options that flex without friction. Consumers with credit cards or other debt, where 42% prioritise savings over 31% debt worry, crave consolidation that frees cash for buffers,add three-month expense projections to seal the deal. Debt-free prospects 61% savings top, build your future list; send them rate updates and early approval events to keep them warm.

Mortgage Brokers Who Adapt Will Own 2026

From a lender partnership angle, prioritise funders who grasp commercial realities: 100% offsets, seamless redraws, and policies that reward buffer-builders without punishing prudence. As 2026 unfolds, with inflation stubborn and rates unpredictable, the savings pivot creates fresh demand for advisers who can structure resilience into every loan. Brokers ready for buffer time now, and fix up later to keep their spot. The residential market isn’t roaring back, but it’s realigning. Borrowers are ready to invest in security, carefully. Match that focus with offset-led strategies and cashflow modelling, and you’re not just arranging loans – you’re architecting mortgage outcomes that win loyalty for years.