12/02/2025

What Brokers Need to Know

In recent insights shared by the Australian Broker, self-managed super funds (SMSFs) are becoming an increasingly popular option for Australians seeking more control over their retirement savings. Unlike traditional industry super funds, where employers dictate how investments are managed, SMSFs allow individuals to take charge of their own funds and make decisions about where to invest. This type of superannuation offers various benefits, including tax advantages and the ability to borrow money within the SMSF to purchase property.

Strong Growth and Rising Demand

The growth of SMSFs has been notable in recent years. As of June 2024, the number of SMSFs in Australia reached 625,609, up from 563,474 in June 2019, according to the Australian Taxation Office. Market research firm IBISWorld has also reported that over the past five years, assets in the SMSF sector have grown at an annualised rate of 1.3%.

Why Australians Are Turning to SMSFs

One of the key drivers behind the rise of SMSFs is the desire for higher returns and more control over personal finances. Chris Hall, founder and managing director of Sydney-based brokerage Blue Crane Capital, highlighted that more people are seeking to take control of their superannuation. Many Australians now prefer to manage their life savings themselves rather than entrusting them to someone else.

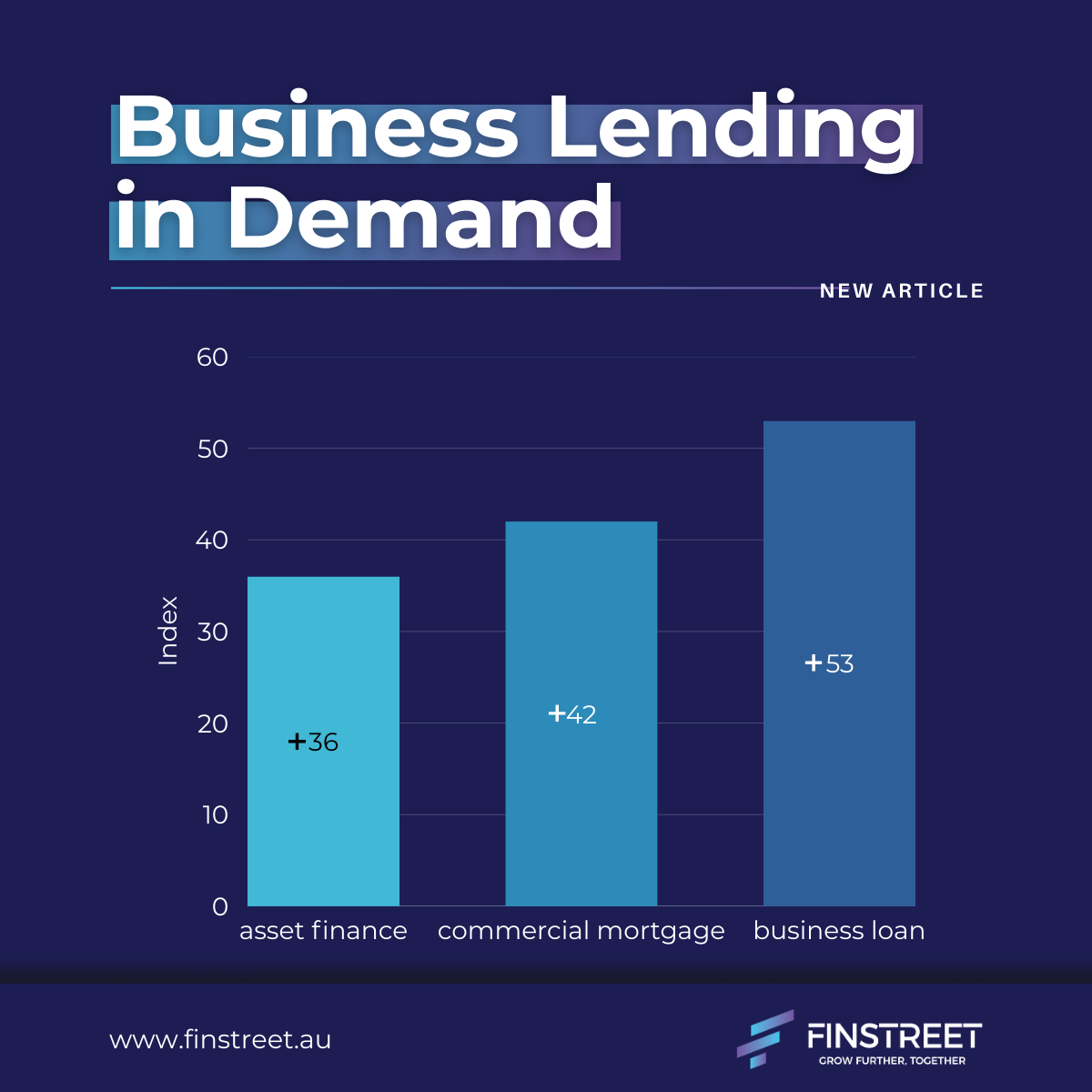

Increasing Interest in SMSF Lending

The increased demand for SMSFs has also been evident in the lending space. Bluestone Home Loans began offering SMSF lending two years ago, and it now represents about 12% of their lending business. According to Tony MacRae, Bluestone’s chief commercial officer, there has been a significant increase in new entrants providing SMSF lending, indicating the growing popularity of this option.

The Benefits of SMSFs: Flexibility and Tax Advantages

The benefits of SMSFs are clear, particularly when it comes to flexibility and control. Business owners who are also tenants can purchase their business property through an SMSF, which offers various tax advantages. Members of an SMSF can borrow up to 80% of the value of residential property and up to 70% for commercial property within the fund. This arrangement allows individuals to make investments that are in line with their goals while also providing substantial tax benefits down the track.

Rules and Restrictions on SMSFs

However, there are rules to be mindful of when managing an SMSF. Funds can only be used for investment purposes, and they cannot be accessed for personal use until retirement age. This is a crucial aspect of managing an SMSF, as it requires discipline and a long-term view.

Property Investment Through SMSFs

The use of SMSFs for property investment is particularly popular among self-employed individuals. Matthew Porch, head of distribution at private lender Aquamore Finance, noted that many self-employed clients are using SMSFs to purchase business premises and rent them back to themselves. This arrangement allows them to manage their investment while building equity for their retirement, rather than paying rent to someone else.

Understanding the Complexities of SMSFs

While SMSFs offer many advantages, they also come with complexities that brokers and lenders must be aware of. Despite being self-managed, SMSFs are still heavily regulated by the government. Alissa Childs, co-founder and mortgage broker at Two Birds One Loan, explained that SMSFs are audited annually to ensure that the funds are being used correctly. If not managed properly, there are risks involved, including the potential loss of superannuation funds due to poor investment decisions.

Navigating the Challenges of SMSF Loans

Childs also pointed out that the structure of SMSFs can be more complicated than standard residential transactions. Brokers must have a solid understanding of the SMSF setup, including the roles of the borrower and the titleholder of the property. Interest rates on SMSF loans are often higher than standard loans, and the paperwork involved can be extensive, making the process time-consuming. Brokers may shy away from SMSFs because of the complexity and the high level of documentation required. Moreover, SMSF loans tend to be harder to refinance due to the high setup costs, making them a more challenging product for brokers to manage.

Weighing the Pros and Cons of SMSFs

SMSFs are an attractive option for Australians looking for more control and flexibility in managing their retirement savings. While they offer significant benefits, including tax breaks and the ability to borrow within the fund, they also come with regulatory complexities and risks. Brokers who work with SMSFs need to be well-versed in the structure and requirements to ensure they provide the best advice and support to clients seeking to manage their superannuation in this way.

Find out more about our SSF products: https://finstreet.au/loan-products/smsf/